Watchlist Update - January 2023

My investment approach is simple but not easy:

Research companies and determine whether they’re ‘wonderful’ firms worthy of being held for a long period of time.

Track the companies that meet my ‘wonderful’ criteria and wait for them to get to an attractive valuation. If they’re still wonderful, buy.

Sell when they’re egregiously overvalued. Alternatively, sell when the business is no longer wonderful - i.e., I made a mistake.

On this substack, I’ve profiled 37 businesses.

I periodically pick a new firm that looks like it’s superficially wonderful and/or cheap. I research it. I publicly write it up on this substack. If it is actually wonderful, then I add it to my watchlist. If it’s wonderful AND cheap, then I buy it.

So far, I’ve deemed 30 of these businesses to be ‘wonderful’.

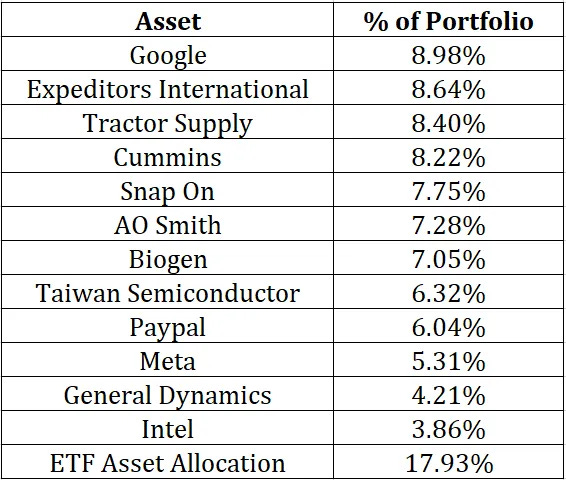

I currently own 12 positions and that make up 82% of my portfolio. Instead of holding cash, I hold my ETF asset allocation strategy.

My goal is to be fully invested with 15 positions. I’m on the hunt for 3 more wonderful businesses that I can buy at wonderful prices.

Valuation: More Art Than Science

What’s a wonderful price?

I look at valuation as a two-pronged approach:

Yield. I want a business that offers a high yield on multiple fronts. I want a high earnings yield. If I were to buy a business privately, then I would want a decent yield relative to what I paid for the entire business. To do this, I flip EV/EBIT into EBIT/EV. For instance, a 10x EV/EBIT multiple translates into a 10% yield. If the EBIT is reliable, recession resistant, and expected to grow in the future, then a 10% yield is a steal. EXPD with a 13.8% earnings yield is a current example of this. I’d also like FCF/EV yields to be high. Additionally, I like to see a high shareholder yield - dividend yield + share buyback yield.

Relative value. I look at the valuation multiples relative to where the stock typically trades. If something usually trades at 9x sales and 6x book, and now it’s at 3x sales and 2.5x book (this is the current situation for META), then I think it’s likely to be a bargain.

If I can get a stock with high yield at a discount to usual trading multiples in a good business, then it’s probably a bargain.

The high yield criteria keeps me from buying stocks that have simply been in a bubble. If a stock trades at a discount to a bubbly multiple, then it’s not really a bargain. Yield keeps me away from the truly bubbly multiples.

The relative value criteria keeps me out of value traps. If a stock always trades below sales, then it’s not actually a bargain just because it’s currently below sales. That’s simply normal for the stock.

The wonderful business criteria is further protection from buying value traps. Good businesses with moats don’t see their earnings and sales evaporate overnight. This is a common occurrence with true value traps. I know because I’ve bought many of them in the past!

The Trojans welcome a value trap in Troy (2004).

I then try to mathematically determine if a combination of yield, multiple appreciation, and business growth over a 10 year period can clear my 10% hurdle.

Why 10%? Simple - I think my ETF asset allocation strategy can deliver a 10% CAGR over the long haul. If I can’t make more than 10% in a stock over 10 years, then I might as well hold my ETFs which require no work, research, monitoring, hair loss, Pepto Bismol, nail biting, etc.

I periodically run through my watchlist of profiled wonderful companies and look at their valuations. This is the current list.

The Watchlist