Thermo Fisher Scientific (TMO)

Key Statistics

EV/EBIT = 24.4x

ROE = 13.75%

Debt/Equity = 69%

FCF Yield = 3.6%

Dividend Yield = .43%

Market Cap = $152.06 billion

The Company

Thermo Fisher Scientific (TMO) provides scientific equipment, laboratory supplies, and specialized services to hospitals, research labs, and academic institutions. They make advanced testing machines, chemical materials, and research tools that scientists use to study diseases and develop new medicines.

Thermo Fisher Scientific was created in 2006 through the merger of two major players in the scientific industry: Thermo Electron and Fisher Scientific.

Thermo Electron was founded in 1956 by George Hatsopoulos, a Greek-American engineer who had a deep passion for thermodynamics and technology. Hatsopoulos, who earned a Ph.D. from MIT, built Thermo Electron into a leader in high-tech scientific instruments.

In its early days, Thermo Electron focused on products that converted heat into useful energy, tapping into the fundamental ideas of thermodynamics. One of their first major products was the thermoelectric generator, a device that could turn waste heat into electricity using the Seebeck effect—a scientific principle where a difference in temperature across a material creates a voltage. These generators were crucial for remote locations where dependable electricity was needed.

Another important early invention was the differential scanning calorimeter (DSC), an instrument used to study how materials respond to temperature changes. It became an essential tool for researchers working in materials science, chemistry, and drug development. Throughout the 1960s and 1970s, Thermo Electron continued to innovate by introducing gas analyzers, spectrometers, and radiation detectors, expanding into industries like energy, environmental science, and healthcare.

Meanwhile, Fisher Scientific had been paving its own path. Founded in 1902 by Chester Garfield Fisher in Pittsburgh, Pennsylvania, the company was created to meet the growing demand for laboratory supplies in science and medicine. Fisher recognized the need for a reliable source of lab equipment, chemicals, and glassware, and quickly built a trusted brand.

Early on, Fisher Scientific offered basic but critical lab items—beakers, test tubes, microscopes, and chemical reagents—that were essential for university and industrial laboratories. One of its breakthrough products was a standardized line of laboratory chemicals, making experiments more consistent and reliable. Fisher also became known for precision glassware, including thermometers and volumetric flasks, which were crucial for accurate scientific measurements.

By the mid-20th century, Fisher Scientific had expanded alongside the booming scientific research industry, serving hospitals, universities, and industrial labs. Its extensive catalog became a must-have in laboratories across the country, offering everything from simple glassware to advanced new instruments.

The merger of Thermo Electron and Fisher Scientific in 2006 combined Thermo’s high-tech instrument expertise with Fisher’s distribution power. Together, they formed Thermo Fisher Scientific—a company capable of serving almost every need in the world of scientific research and healthcare.

After the merger, Thermo Fisher grew rapidly, fueled by a series of strategic acquisitions that expanded its reach. In 2014, the company made one of its biggest moves by acquiring Life Technologies, a leader in genetic research and biotechnology. This deal helped Thermo Fisher become a powerhouse in genomics, molecular biology, and next-generation DNA sequencing, opening new doors into personalized medicine and agricultural biotechnology.

In 2011, it acquired Phadia, a company that specialized in allergy and autoimmune disease diagnostics. In 2017, it bought Patheon, a pharmaceutical development and manufacturing firm, strengthening its capabilities in drug production. In 2021, Thermo Fisher acquired PPD, a global contract research organization (CRO), allowing it to expand deeper into clinical research services and help bring new drugs to market more quickly.

These acquisitions, along with many smaller ones, transformed Thermo Fisher from a company focused mainly on scientific instruments and lab supplies into a diversified leader across diagnostics, life sciences, healthcare, and industrial research.

Today, Thermo Fisher Scientific operates through four major business segments: Life Sciences Solutions, Analytical Instruments, Specialty Diagnostics, and Laboratory Products and Biopharma Services.

The Life Sciences Solutions segment contributes about 21.5% of Thermo Fisher’s total revenue. It provides essential tools—like reagents, instruments, and lab materials—that scientists use for biological research, diagnosing diseases, and developing new drugs and vaccines. Customers include pharmaceutical companies, biotech firms, hospitals, universities, and government agencies. Within this segment, Biosciences supplies tools for studying cells and proteins, Genetic Sciences provides advanced equipment for DNA and genetic research, and BioProduction supports drug makers with specialized products to help manufacture vaccines and biologic medicines.

The Analytical Instruments segment brings in about 17% of the company’s revenue. This part of the business sells sophisticated lab instruments, consumables, and software that scientists and industries use for everything from routine testing to advanced research. Customers include pharmaceutical companies, academic researchers, government labs, and environmental scientists. Analytical Instruments includes Chromatography and Mass Spectrometry machines, which analyze chemical and biological samples; Chemical Analysis tools, used for industrial safety and environmental monitoring; and Electron Microscopes, which provide incredibly detailed images of cells, materials, and semiconductor components.

Specialty Diagnostics accounts for around 10% of Thermo Fisher’s revenue. This segment focuses on medical testing and healthcare, providing products that help doctors and labs diagnose diseases quickly and accurately. It offers tests for drug monitoring, cancer detection, allergy and asthma diagnosis, and infection control. Specialty Diagnostics also supports organ transplant matching through genetic testing and supplies hospitals and clinical labs with everyday medical supplies, helping improve healthcare quality while keeping costs down.

The Laboratory Products and Biopharma Services segment is the largest and most important part of Thermo Fisher’s business, making up nearly 52% of total revenue. This segment plays a critical role in supporting scientific labs and pharmaceutical companies. It combines the sale of everyday lab supplies—like beakers, gloves, test tubes, and high-purity chemicals—with a wide range of professional services that help companies develop, test, and manufacture new drugs.

One key area within this segment is Laboratory Products, which provides all the physical supplies that labs need. Another is the Research and Safety Market Channel, which acts as a massive distribution center, offering Thermo Fisher’s products alongside supplies from other brands, giving labs easy access to everything they require.

On the pharmaceutical side, Pharma Services helps drug companies manage the challenging parts of developing new medicines. It handles large-scale manufacturing, quality control, and supply logistics, helping companies get new treatments to market faster and more efficiently. The Clinical Research business provides full support for clinical trials, guiding clients through every phase of drug testing, from early human trials to post-approval monitoring.

The COVID-19 pandemic gave a major boost to Thermo Fisher’s business. Demand for diagnostic tests, lab equipment, and vaccine production supplies skyrocketed, driving record sales in 2020 and 2021. Thermo Fisher played a key role by supplying COVID-19 testing kits, vaccine raw materials, and cold storage equipment.

However, as the pandemic eased, demand for COVID-specific products dropped. While core business areas like biopharma services and life sciences remain strong, overall earnings growth has slowed compared to the peak pandemic years.

Performance

Thermo Fisher’s stock has delivered impressive long-term returns. From 2007 through the end of 2024, it achieved a compound annual growth rate (CAGR) of 14.87%, turning a $10,000 investment into $121,169.91. This significantly outpaced the S&P 500, which delivered a 10.3% CAGR over the same period.

For much of its history, Thermo Fisher’s stock drawdowns have generally tracked those of the broader market. It experienced a 50% decline during the 2008 financial crisis, similar to the S&P 500. The stock also fell sharply during the COVID-19 selloff in March 2020 and declined again alongside the market during the 2022 bear market.

However, in 2023, Thermo Fisher underperformed the broader market, suffering a 35% drop. This steeper pullback was largely due to a sharp decline in demand for COVID-19 testing products, which had significantly boosted revenues during the pandemic. Investor sentiment and valuation also swung dramatically in response to these shifts. The price-to-sales multiple surged from 3.7x in 2018 to 6.7x by the end of 2021, as investors priced in pandemic-driven growth, before normalizing to 4.6x by the end of 2024 as COVID-related revenues faded and growth rates returned to more sustainable levels.

Although the stock has partially recovered, it remains in a 20% drawdown from its all-time highs.

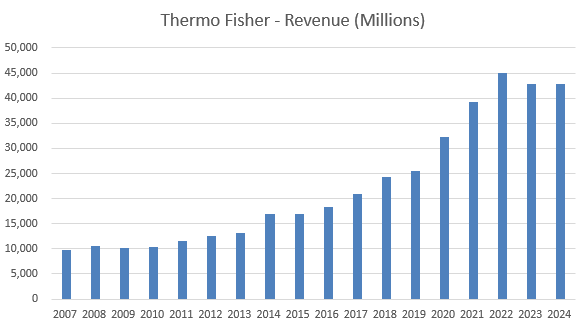

Much of Thermo Fisher’s strong stock performance has been fueled by consistent revenue growth. From 2007 to 2024, revenues climbed from $9.7 billion to $42.8 billion, growing at a compound annual rate of about 9%.