Portfolio Management Guidelines: Position Sizing, Alternative to Cash, & Sell Rules

Portfolio Management

This substack is primarily to publish my write-ups of companies.

I am looking for companies with attractive economics that are worthy of being held for the long-term. I am then attempting to acquire them at an attractive price.

Left from the ‘buy/pass’ decisions are how I actually manage the portfolio.

My buy rules are straightforward and outlined in this checklist, which I go through for each stock purchase.

On this substack, I have not discussed how I think about position sizing and what I do when I can’t find stocks that meet my strict criteria.

Position Sizing & My Issues With Deep Value

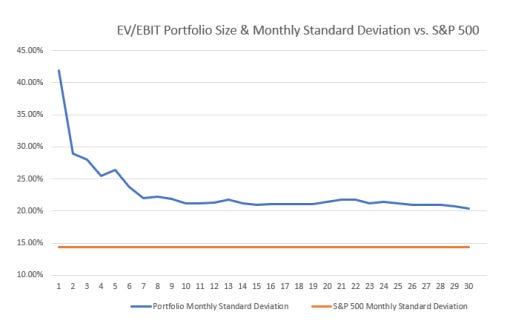

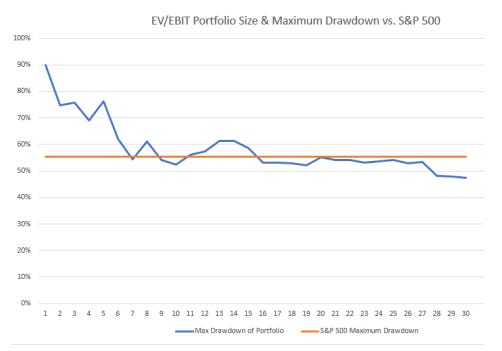

My research shows that a bulk of the benefits of diversification happens with the first dozen positions and appears to be maximized around 15. For this reason, my goal is to be fully invested in 12-15 positions meeting my criteria.

Each additional position adds an increasingly declining marginal benefit to reducing volatility and drawdowns.

In the past, I’ve attempted to manage a much bigger portfolio (over 20 positions) and found it difficult to manage and continually generate new ideas.

Investing is a part-time endeavor for me. Keeping up with 20-30 companies was extremely difficult and the added effort didn’t help my returns. It only added to my personal stress.

The effort to fill up a portfolio with over 20 positions also resulted in me pursuing sub-par ideas. The reality of markets is that companies meeting my strict criteria are hard to come by unless we’re in a panicky market.

When I was managing a 20+ stock portfolio, I was also more of a deep value investor. I was flipping sub-par companies when they were undervalued, selling when they were fairly valued. This is a frenetic endeavor that I did not really enjoy.

Due to the low quality of the companies, I also needed to have a strong opinion about the economic cycle. Were we in the early trough of an economic cycle, in which case deep value would do extremely well? Were we at the peak of an economic cycle, in which case deep value stocks were only optically cheap because they were over-earning? If we’re only in the early stages of a recessions, should these companies be sold? I lost a lot of sleep worrying about these issues.

These days, my belief is that the economic cycle is mostly unpredictable and that my efforts to determine our place in the economic cycle were fruitless and a waste of time. Much of my insight into the economic cycle were derived from historical comparisons. Unfortunately, a template that worked in a previous boom-bust cycle never quite works in the next boom-bust cycle. Every mega-bear market has its own unique flavor and history never quite repeats itself, making them nearly impossible to predict & time.

For these reasons, I don’t want to heavily trade sub-par companies. I want to identify companies that are worthy of being held, not traded.

There is nothing inherently wrong with a deep value style. In fact, the research indicates that it leads to superior returns. However, I found it difficult to manage as an individual part-time investor.

Additionally, I think that a better vehicle for a deep value strategy is through an ETF. Examples are standard small-cap-value ETF’s like VBR and SLYV. There are more concentrated strategies, available in ETF’s like DEEP or QVAL. If an investor prefers deep value, I think that the effort can be outsourced to an ETF. One of these ETF’s can be put on a shelf for 20 years at a low expense ratio and low stress. If held in a taxable account, the tax consequences are also optimized. Taxes don’t need to be paid when each position is sold. They only need to be paid when the ETF itself is sold.

For this account, my goal is to be invested in at least 12 wonderful companies and maxing out the portfolio size at 15. I think that this is manageable for a part-time investor like myself.

When initially buying a stock, I make a decision between whether this will be a 1/12 position (8.33%) or 1/15 position (6.67%). This decision is made based on the undervaluation of the company combined with the uncertainty of the situation. A deeply undervalued company that I feel has an incredible moat (such as Google right now or General Dynamics in fall 2020), will earn itself a 8.33% position.

I don’t make “YOLO” trades or invest massive percentages of the portfolio in single ideas due to conviction. I have been investing for over 20 years. In that time, I’ve never been able to actually identify the best performing stock in my portfolio in advance. I believe that efforts to concentrate in a ‘best idea’ are misguided at best and can lead to ruin at worst.

An Alternative to Cash

I don’t hold any cash and hold the ‘weird portfolio’ instead. This is by design.

In the past, I’ve attempted to hold large quantities of cash while I waited for opportunities. The problem with this is that cash earns nothing. I often found that the cash was ‘burning a hole in my pocket’ and compelled me to buy stocks that didn’t meet all of my criteria.

Years ago, I designed an asset allocation model for myself that I could pile my savings into. I dubbed this the “weird portfolio” and I wrote a book about it which you can read for free here.

This is my version of a permanent portfolio, though it is much more aggressive and targeted than Harry Browne’s version. The idea is to hold equally weighted asset classes and have zero opinion about timing the market cycle.

I own the asset classes via ETF’s. The asset classes that I use are:

US Small Cap Value

International Small Caps

Real Estate

Gold

Long Term Treasuries

The goals of this portfolio are as follows:

Achieve a 4-7% rate of return exceeding the rate of inflation.

Limit drawdowns to 2/3 of the US stock market’s maximum drawdown.

Avoid lost decades. I want to avoid the boom-bust tendency of large cap, market cap weighted indexes.

Minimize fees & taxes.

Use passive products that do not rely on the genius of a manager whose genius will probably fade.

Avoid the need for macroeconomic predictions or market calls.

This asset allocation gives me an opportunity to invest when I can’t find individual stocks that meet my strict criteria.

Throughout the last two years, I had nearly 3/4 of my account in this asset allocation because there were so few opportunities in the market. Having nearly 3/4 of my account in cash would have been disastrous, but the asset allocation provided a satisfactory return. I earned 14.54% in the asset allocation model last year, which certainly beats near-0% cash. In fact, if I were mostly in cash, I don’t believe that I would have been able to stay there for long due to the temptation to swing at sub-par opportunities.

Additionally, while the S&P 500 declined by over 10% this year and the Nasdaq 100 entered a bear market, this account was only down 5%. This gave me ammunition to buy wonderful companies as they began to fall to wonderful prices. The panic in the markets has been an opportunity for me to seize.

All of these asset classes can be accessed cheaply in liquid ETF’s.

The liquidity is advantageous. As soon as I identify an opportunity, I can quickly sell some of my ETF’s and purchase the business that I am interested in.

Sells

I am not a ‘never sell’ investor who will hold companies indefinitely, though my preference is to hold for the long-term. I give myself the flexibility to sell if necessary.

Reasons to sell are listed below:

The stock has reached an extreme valuation relative to its history.

A more compelling bargain is available.

The business has lost its competitive advantage.

To limit a stock that has grown to be too large a percentage of the overall portfolio.

If a stock meets even one of the above criteria, I will consider selling. Usually, there will be multiple criteria on this list that will overlap.

Goals

Ultimately, my goal is to be fully invested in 12-15 wonderful companies, acquire them at wonderful prices, and hold for long periods of time.

I set out to accomplish this goal in 2020. It has taken 2 years to build this account up to being 1/2 invested, with a bulk of this buying occurring during the recent market panic.

Throughout the market cycles, I will continue to analyze companies and determine if they are worthy of being held. When they reach attractive valuations, I will buy, as I have been doing recently.

Disclaimer

Nothing on this substack is investment advice.

The information in this article is for information and discussion purposes only. It does not constitute a recommendation to purchase or sell any financial instruments or other products. Investment decisions should not be made with this article and one should take into account the investment objectives or financial situation of any particular person or institution.

Investors should obtain advice based on their own individual circumstances from their own tax, financial, legal, and other advisers about the risks and merits of any transaction before making an investment decision, and only make such decisions on the basis of the investor’s own objectives, experience, and resources.

The information contained in this article is based on generally-available information and, although obtained from sources believed to be reliable, its accuracy and completeness cannot be assured, and such information may be incomplete or condensed.

Investments in financial instruments or other products carry significant risk, including the possible total loss of the principal amount invested. This article and its author does not purport to identify all the risks or material considerations that may be associated with entering into any transaction. This author of this website accepts no liability for any loss (whether direct, indirect, or consequential) that may arise from any use of the information contained in or derived from this website.