LKQ Corporation (LKQ)

Key Statistics

EV/EBIT = 12.6x

ROE = 11.37%

Debt/Equity = 95%

FCF Yield = 4.29%

Dividend Yield = 3.23%

Market Cap = $9.59 billion

The Company

LKQ Corporation (LKQ) is a global company specializing in the sale of used, recycled, and aftermarket auto parts.

Instead of selling expensive, brand-new parts directly from manufacturers, LKQ provides more affordable alternatives that are often just as good. These include parts that have been reused from wrecked vehicles, rebuilt, or made by third-party companies. The company serves body shops, mechanics, and car owners across the U.S., Canada, and Europe, making it one of the most prominent and most trusted names in the industry.

The heart of LKQ's business is selling parts and services, which account for approximately 95% of the company’s revenue. These include items such as used bumpers, recycled engines, aftermarket headlights, and services like vehicle diagnostics and hybrid battery repairs. The remaining 5% of LKQ’s revenue comes from things like selling scrap metal, catalytic converter materials, and entry fees at its self-service yards. Even though this "other" category is smaller, it still helps boost profits and reduce waste.

Founded in 1998, LKQ began with a simple goal: to provide customers with high-quality car parts at affordable prices. The name "LKQ" stands for "Like Kind and Quality," showing its focus on selling parts that meet the same standards as original ones. The company began by buying up smaller regional auto recyclers. As it grew, it moved beyond just recycled parts, adding aftermarket and remanufactured components, as well as parts for RVs, off-road vehicles, and even boats.

By the early 2000s, LKQ had gone public and begun expanding beyond the U.S. Its biggest step into Europe occurred in 2011, when it acquired Euro Car Parts in the UK. From there, the company expanded rapidly into Germany, Italy, and other European countries. In 2014, it launched its Self Service segment, where customers could come to a salvage yard and pick their own parts. That same year, it bought Keystone Specialty to enter the performance and accessory market.

Since 2010, LKQ has continued to grow through strategic acquisitions. The Euro Car Parts deal gave it a strong European base. Between 2013 and 2016, it added distributors in countries like Poland, the Czech Republic, and Slovakia. In 2014, it acquired Keystone Automotive to sell specialty parts like towing equipment and off-road accessories. In 2017, it bought Warn Industries, a company that makes winches and bumpers. A major deal was struck in 2018 with the acquisition of Stahlgruber, a significant German parts distributor.

In 2023, LKQ made headlines by acquiring Uni-Select Inc. for $2.1 billion. This gave LKQ full access to FinishMaster, a leader in auto paint and coatings, and the Canadian Automotive Group, a major supplier of parts in Canada. The deal also included a UK company, GSF Car Parts, which LKQ plans to sell off to avoid overlapping with its existing operations. This acquisition helped LKQ expand in both Canada and the paint business.

One of LKQ's biggest strengths is its strong relationship with insurance companies. Like Copart, another auto-related business, LKQ benefits when insurers send wrecked vehicles their way. This provides LKQ with a steady supply of cars to strip for usable parts. These close ties give LKQ a significant advantage over smaller competitors who lack the same connections or purchasing power.

LKQ dominates the alternative auto parts industry. It has very few serious competitors. Some smaller players, like Fenix Parts and Pick-n-Pull, operate regionally. Genuine Parts Company, which owns NAPA Auto Parts, is a global competitor, focusing primarily on new and original equipment manufacturer (OEM) parts. Thanks to its size, efficiency, and strong relationships with insurers, LKQ has built a robust moat that keeps it ahead of the pack.

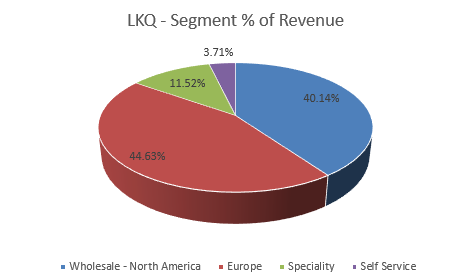

The company is organized into four main business segments.

Wholesale - North America makes up about 40% of LKQ’s revenue. This part of the company supplies body shops and mechanics with used and aftermarket parts, including bumpers, lights, and paint. It also offers services like diagnostics and battery reconditioning. This segment is LKQ's most profitable, with EBITDA margins of 16.6%. LKQ sources parts from the U.S. and Asia and recycles valuable materials like metal and catalytic converters.

The Europe segment accounts for 44.6% of revenue. It operates in about 20 countries and mainly sells parts for vehicles that are 3 to 15 years old. LKQ is starting to add more recycling and remanufacturing to this segment. It also uses private label brands to improve margins. The company sells parts to repair shops through a highly efficient network, and it’s upgrading its tech systems to better manage inventory and customer orders. The Europe segment has EBITDA margins of 9.9%.

The Specialty segment brings in about 11.5% of LKQ’s revenue. This part of the business sells accessories and high-performance parts for RVs, trucks, and boats. Customers include small businesses, online retailers, and individual enthusiasts. Popular items include towing hitches, marine electronics, and off-road gear. LKQ sources these products mainly from the U.S., Canada, and China. Most sales happen online, and the segment is supported by an extensive delivery network. It runs with EBITDA margins around 6.8%.

Finally, the Self-Service segment, also known as "Pick Your Part," accounts for approximately 3.7% of revenue. Here, customers pay a small fee to enter a salvage yard and remove parts themselves from old vehicles. LKQ also sells leftover scrap metal, fluids, and valuable parts, such as catalytic converters. The vehicles come from auctions, insurance companies, and the public. Cars usually stay in the yard for up to four months before they’re crushed and recycled. This segment earns solid EBITDA margins of 9.4%.

Performance

From 2003 through the end of 2024, LKQ delivered a compound annual growth rate (CAGR) of 15.43%, turning a $10,000 investment into over $210,000—significantly outperforming the S&P 500, which returned a 10.58% CAGR over the same period.

Despite this long-term success, the stock has been volatile. LKQ saw a 60% drawdown during the global financial crisis, roughly in line with the S&P 500’s 50% drop. It regularly experiences 20–30% pullbacks, often due to investor overreactions to earnings reports.

One of its largest declines came between 2017 and March 2020, when the stock fell 68% due to softening demand, falling used car prices, and the onset of the COVID-19 pandemic. Lockdowns reduced driving and vehicle repairs, while salvage pricing and supply chain disruptions hurt profitability.

As of now, the stock is in a 33% drawdown, largely triggered by tariff concerns and a weaker-than-expected Q1 2025 earnings report. Revenue dropped 6.5% year-over-year, and free cash flow turned negative. Tariffs on imported parts—especially from Asia—threaten to raise costs on 10–30% of LKQ’s product base.

In response, management formed a “Tariff Task Force” to mitigate risks, maintain margins, and protect full-year guidance.